Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

I get an apologetic phone call from clients now and then, and I think its kind of sweet. They don’t want to transact but have a question they know I can answer, and feel like they are imposing. Post sale service is a legitimate thing to me, and I always tell them that their call is a welcome one. Every agent wants to stay top of mind with their past client if they have half a brain, and these “impositions” are anything but.

I get an apologetic phone call from clients now and then, and I think its kind of sweet. They don’t want to transact but have a question they know I can answer, and feel like they are imposing. Post sale service is a legitimate thing to me, and I always tell them that their call is a welcome one. Every agent wants to stay top of mind with their past client if they have half a brain, and these “impositions” are anything but.

So if you own a home and you have a question that you think your real estate agent can answer, please don’t ever be shy about asking just because you aren’t calling them to buy or sell right now. It’s more than fine, a good agent will want to help in any way they can.

A few good reasons to call your agent, even if you are years if not decades away from listing your home for sale are as follows:

- Getting your home value updated. I’ve said this before, but knowing your home’s estimated value is good for more than putting it on the market. You might want to grieve your property taxes. Knowing your equity position for a line of credit is always a great idea, especially if you are considering home improvements.

- Home Improvements Return on Investment. The idea of renovating, expanding, or otherwise improving your property will likely raise your value. Your agent can give you a sense of how much that value potentially is, and weigh it against the time you plan on staying and the expense of the work.

- The Golden Rolodex. Over the years I have had savvy clients pick my brain about referrals for non- transaction related services, and with good reason. I know the contractors. I know the lawyers. I know all the good places to eat, shop, and who’s who in the community. I have referred clients to all kinds of contractors, estate planning attorneys, auto mechanics, wedding venues, and all sorts of community services from Little League to Meals on Wheels. A good agent always has a guy for that.

- Finding other agents outside the market. Smart clients of mine have often asked me if I know a good agent out of state for a friend or relative considering moving. Without exaggerating, I have probably played matchmaker to grateful strangers in at least 30 of the 50 states over the years. I’m in a number of networks outside my own sphere to fill in the gaps but I’m proud of the connections I have facilitated.

There are plenty of other reasons, but I think you get the point. A friend once told me that real estate agents are the welcome wagon of most communities, and I totally agree. You real estate agent is a valuable resource, and you should never hesitate to reach out to them if you think they might be able to shed some light on anything for you.

You can still buy a nice 3 bedroom home in Putnam County for under $350,000 like the one our buyer client closed on last week. It is a fully renovated 1100 square foot 3 bedroom, 2 bath bungalow on a level lot with parking for at least 4 cars. The siding, roof, HVAC, walls, kitchen, and baths are all new. It is in the Putnam Lake community, so the property has lake rights- as a matter of fact the water is only about 500 feet from the front door. Putnam Lake (or “Put Lake,” as the locals and agents affectionately refer to it) is a woodsy, sleepy community of tidy homes that tend to be on the smaller side, so it is a great place for starter homes for anyone who likes lake living. There is shopping and food nearby, and the area is served by the Brewster school district.

You can still buy a nice 3 bedroom home in Putnam County for under $350,000 like the one our buyer client closed on last week. It is a fully renovated 1100 square foot 3 bedroom, 2 bath bungalow on a level lot with parking for at least 4 cars. The siding, roof, HVAC, walls, kitchen, and baths are all new. It is in the Putnam Lake community, so the property has lake rights- as a matter of fact the water is only about 500 feet from the front door. Putnam Lake (or “Put Lake,” as the locals and agents affectionately refer to it) is a woodsy, sleepy community of tidy homes that tend to be on the smaller side, so it is a great place for starter homes for anyone who likes lake living. There is shopping and food nearby, and the area is served by the Brewster school district.

Decades ago when I was tending bar, we always knew to avoid any discussion of politics or religion because it was a powder keg. In real estate, that would also include any discussion involving Zillow, dual agency, and square footage.

Decades ago when I was tending bar, we always knew to avoid any discussion of politics or religion because it was a powder keg. In real estate, that would also include any discussion involving Zillow, dual agency, and square footage.

The term “in law apartment” or “in-law space” has become misunderstood lately by both agents and consumers, so I’d like to clear up what should be fairly straightforward.

The term “in law apartment” or “in-law space” has become misunderstood lately by both agents and consumers, so I’d like to clear up what should be fairly straightforward.

If I were asked by a seller what separates me from other agents to get them the best price for their home, I’d answer their question with a question of my own.

If I were asked by a seller what separates me from other agents to get them the best price for their home, I’d answer their question with a question of my own.

Westchester County has a population of about 1 million residents. Most of those folks who inhabit the 914 area code live in homes that are connected to public sewers, but there are a hefty number of properties, especially in the northern part of the county, that are on septic systems. I’ve

Westchester County has a population of about 1 million residents. Most of those folks who inhabit the 914 area code live in homes that are connected to public sewers, but there are a hefty number of properties, especially in the northern part of the county, that are on septic systems. I’ve

I

I

Ever since I got in to real estate in the 90s, the public has had a bit of a preoccupation with buying foreclosures. The perception that a bank owned property is a bargain is hard to argue with, but it’s not always a simple or straightforward process. Having specialized in distressed properties for decades, I’ll share some things that buyers really need to know before they purchase something around these parts, because New York is a different animal, and Westchester and the surrounding counties are not like upstate either.

Ever since I got in to real estate in the 90s, the public has had a bit of a preoccupation with buying foreclosures. The perception that a bank owned property is a bargain is hard to argue with, but it’s not always a simple or straightforward process. Having specialized in distressed properties for decades, I’ll share some things that buyers really need to know before they purchase something around these parts, because New York is a different animal, and Westchester and the surrounding counties are not like upstate either.

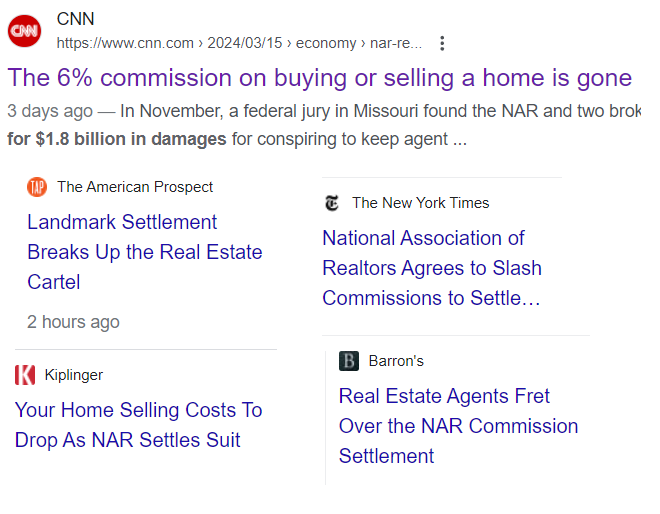

When I went to pick my son up from baseball practice earlier this week, a friend came up an smiled at me. “Sorry about your pay cut!” I knew what she was referring to, and as I peruse the news reports on the recent NAR commission settlement, I share many other Americans’ frustration at the failure of our journalism to accurately report on the matter. I know racy headlines get clicks and sell papers, but accuracy in reporting is still important.

When I went to pick my son up from baseball practice earlier this week, a friend came up an smiled at me. “Sorry about your pay cut!” I knew what she was referring to, and as I peruse the news reports on the recent NAR commission settlement, I share many other Americans’ frustration at the failure of our journalism to accurately report on the matter. I know racy headlines get clicks and sell papers, but accuracy in reporting is still important.

If you’re my age or older, you probably recall the the old Dick Van Dyke show. Dick Van Dyke Played Rob Petrie and his TV wife Laura was played by the great Mary Tyler Moore. You may not recall the exact address, but the Petrie family lived at fictitious 148 Bonnie Meadow Road, New Rochelle. Bonnie Meadow Road actually does exist! 9 out of 10 Westchester residents over the age of 50 know the show was set in New Roc, but even I didn’t know the address.

If you’re my age or older, you probably recall the the old Dick Van Dyke show. Dick Van Dyke Played Rob Petrie and his TV wife Laura was played by the great Mary Tyler Moore. You may not recall the exact address, but the Petrie family lived at fictitious 148 Bonnie Meadow Road, New Rochelle. Bonnie Meadow Road actually does exist! 9 out of 10 Westchester residents over the age of 50 know the show was set in New Roc, but even I didn’t know the address.

If you’ve ever wondered what the story is behind those flimsy looking signs nailed to telephone poles all over the place promising you a fast cash sale on your house, I have the answer.

If you’ve ever wondered what the story is behind those flimsy looking signs nailed to telephone poles all over the place promising you a fast cash sale on your house, I have the answer.

If your budget is in the $700,000 range and you’re looking in Ossining, you’ll be pleased to know that you can still buy a 4 bedroom home on over an acre like the one we just closed on this week in town. 5 Ridgeview drive has 4 bedrooms, 3 baths, and a 1.6 acre lot.

If your budget is in the $700,000 range and you’re looking in Ossining, you’ll be pleased to know that you can still buy a 4 bedroom home on over an acre like the one we just closed on this week in town. 5 Ridgeview drive has 4 bedrooms, 3 baths, and a 1.6 acre lot.

Swimming pools are probably the last thing on most peoples’ minds but we are still selling homes that have them, and this thought is a bit overdue.

Swimming pools are probably the last thing on most peoples’ minds but we are still selling homes that have them, and this thought is a bit overdue.

When I was first licensed in the 1990s, if a house didn’t sell for a period of time like 30 or 60 days, we would often reduce the price. Sometimes it was because we had too few showings, or because the showings we had didn’t yield any offers. On occasion, some home sellers would voice concern at a price change because no one had seen the house to give them price feedback. We’d have to explain that the feedback was the actual absence of showings. It wasn’t a truly data-driven process, however, because we had no means of measuring who saw the house either through their agent’s analog means (like seeing it in a broker’s binder) or advertised in publications and passed on it. We did have ample evidence that once a price was reduced, that the market responded.

When I was first licensed in the 1990s, if a house didn’t sell for a period of time like 30 or 60 days, we would often reduce the price. Sometimes it was because we had too few showings, or because the showings we had didn’t yield any offers. On occasion, some home sellers would voice concern at a price change because no one had seen the house to give them price feedback. We’d have to explain that the feedback was the actual absence of showings. It wasn’t a truly data-driven process, however, because we had no means of measuring who saw the house either through their agent’s analog means (like seeing it in a broker’s binder) or advertised in publications and passed on it. We did have ample evidence that once a price was reduced, that the market responded.

Back in 2009, I was approached by Redfin to help them enter the Westchester real estate market as a referral partner. They did not have employee agents here, so referring clientele to other brokerages would be a win/win arrangement to start. I was eager for any new source of business, and took a closer look. Part of their vetting process was to survey my past clients, which was fine, but to also publish my client’s reviews online.

Back in 2009, I was approached by Redfin to help them enter the Westchester real estate market as a referral partner. They did not have employee agents here, so referring clientele to other brokerages would be a win/win arrangement to start. I was eager for any new source of business, and took a closer look. Part of their vetting process was to survey my past clients, which was fine, but to also publish my client’s reviews online.

Escalation Clauses in Offers to Purchase: a Double Edge Sword

The first escalation offer I can recall was a sale I made in 2012. The house was a rare offering and the market was, at long last, recovering, and the winning bid promised to be $2500 higher than any superior offer. The listing was sold for about $40,000 over asking, and that clause made the difference for the buyer who ended up getting the house. That buyer was paying cash, so it was a particularly strong proposal in the terms category as well as price.

When the market heated up around 2020, escalation clauses became far more common. Not many listing agents understood them well enough to properly convey the message to their seller clients as effectively as they could have, but by 2021 most agents grasped the mechanics.

Unfortunately, some agents know them a little too well. Yes, escalation clauses are no longer viewed as obscure or a gimmick, but they aren’t always the answer. Here are a few scenarios where they just don’t work the way the presenting agent thinks they will:

It has gotten to the point where some listings will state that no escalations will be entertained. We recently had a multiple offer situation on a listing where the winning bid was chosen because it had a high down payment and waived the appraisal contingency. An offer with a VA mortgage came in with an escalation clause, but VA mortgages are 100% financing, or 0 down. That might have gotten the seller an additional $5,000, but the risk of going to contract with a buyer with no cash to cover an under appraisal was not palatable for the seller. The buyer agent was unhappy about this, and I do appreciate the uphill battle VA buyers face, but that agent did not have an answer for the possibility of an appraisal problem.

Escalations can indeed make a difference. But they aren’t the panacea that some think they are because of the law of unintended consequences connected to other terms, and agents need to educate their clients that the clause isn’t a magic wand.