I don’t think I’ve seen the following thought written anywhere lately, but I’ll say it:

The average real estate agent has never worked harder than they have in this market.

That seems contrary to the public perception that rising prices and a “hot” market is when agents have it easy, but extreme conditions aren’t conducive to a leisurely business model.

For example, when an agent sells their new listing the first weekend that it’s active for more than asking, it not only doesn’t mean things are easier for them, it can have a deleterious effect on their bottom line.

Listing agent challenges include:

More difficulty procuring the listings. Competition is higher for the listing, and many homeowners need a plan on where they’ll go once they sell because that’s the biggest challenge. You have to have a detailed plan in beyond the sale, which is unheard of in any market I’ve ever seen before this one. Before this market the plan was “find a place to buy/move to.”

Bidding wars aren’t fun, and can get messy. The passions around housing are high enough, but try explaining to a colleague why their cash offer $50,000 over asking is in 3rd position. And there is no margin for error, as the devil is often in the details on offers, and missing a key term can cost. If you meet an agent with bags under their eyes, they were likely parsing the details of 6-10 offers with a nervous client to help them make a decision.

Appraisals can be a nightmare. When prices spike dramatically, the 6 month lookback at comparable sales is at lower cost transactions. Buyers can offer cash protection, but it’s not automatic and an appraisal $25,000 under contract price can spark some serious buyer remorse that reverberates to all parties.

Greed. Sellers view the current market as a once in a lifetime chance to ring the bell, but it can blur their common sense and cause them to have unrealistic expectations even if everything goes right. For example, suppose a listing goes active for $800,000 and sells for asking price within the first week. Great, right? But if the seller had a fantasy that they’d get $860,000 in a bidding war based on what they see on the news, they need to be talked off a ledge.

Lack of professionalism. There are 1.5 million members of NAR right now, up 50% from the housing crash. That means hundreds of thousands of rookie agents who have no substantive experience. When the market gets hot, old failures take their licenses out of mothballs, and newbies jump in with deplorably sparse training. Doing business with a poorly trained agent on the other side of a deal is brutal.

Loss of income. This is counterintuitive, but all too real. Less inventory spread over a dramatic increase in agents is bad enough, but the big aggregators are getting in on the commission via onerous referral fees. We used to pay for advertising on Zillow, Trulia, and Realtor.com. Now those companies take referral fees of 35% on a typical transaction, meaning that if you sell a $450,000 property your commission is more reflective of a $300,000 closing. So higher prices not only don’t mean more commission, they mean lower earnings spread over fewer transactions.

Other issues are more inside baseball, but the model of the industry has always been predicated on the longstanding idea that carrying a listing for any period of time will develop new prospective client relationships with inquiries on the listing. When the listing is gone the first weekend, that can’t happen. I understand this means little to the consumer, but it’s a factor that can’t be denied.

On the buying side, agents representing prospective purchasers are in trench warfare. Buyer agents in our firm have fewer properties to show their clients, and many of our successful buyers have not hit paydirt until their 4th or 7th attempt to buy. That’s madness. Worse, buyers are selling their souls to get accepted offers by waiving inspections, offering cash to make up for appraisal deficiencies, and in some cases even waiving mortgage contingencies. Surrendering your own security and exposing yourself to that kind of liability is not only stressful and risky, it can be destructive if everything doesn’t go perfectly.

In any industry, volatility is not a welcome thing. Stability, even if it’s considered boring, is a far better market condition. Give me boring any day. Leave the volatility for the Oscars.

Stay tuned for my next post on why this is brutal for consumers as well!

I got a question from a client about the effect that installing solar panels might have on their home’s value. It’s a good question, actually. Years ago when hurricanes knocked out power in our area for more than a week, I opined that backup generators would become the new status symbol. While I wasn’t wrong, green initiatives are gaining momentum and NAR even has a Green Housing certification for agents.

I plan on getting solar power in the near future. I see panels everywhere I go. I’m more interested in saving on my bills and not burning fossil fuels, but it is a good question- will solar panels increase value?

In all candor, this is not something I can speak to clearly on my own- the data is not too plentiful. Of the thousands of homes sold in Westchester in the last year, only a few dozen had solar. I can see why; the technology is relatively new and most people who install solar do so because they aren’t going anywhere anytime soon. So, there really isn’t a statistically significant number locally to go by.

That doesn’t help me answer the client’s question, so I did a little snooping around, and Zillow released a study in 2019 that confirmed that solar raises value by 4.1%. Zillow has way more data to crunch than I do, so there’s you’re answer based on their study. This is hard data and not an algorithm attempting to estimate value sight unseen, so I think the findings are reliable.

As I shared with my client:

My take is that there is no downside, leased or owned. There is no evidence I’ve ever found that said it harmed value. I think as time goes by more data will confirm Zillow’s finding.

I see more and more homes converting, and I’m planning on installing panels later this year so the trend is positive.

Younger buyers also prefer more green solutions and millennials comprise the bulk of the forecast of buyers in the coming years.

I’m relatively old. I remember Nixon resigning office, Tang commercials, news stories on the war in Vietnam, and lots of other things from when Kitchens were green and gold. I remember when mortgage interest rates topped 20% in the early 1980s, and my father telling my mother how rates didn’t matter, payment amounts did. He was an accountant, so he wasn’t playing out of position on that one.

Having lived through two housing crashes in my 54 years, I’ve become a student of what to look for so that what I endured in 2008-10 will never catch me unprepared again. So when I’m asked if rising rates will stall the market, I have to laugh.

A brief, immutable point before I go on:

People like living indoors. It’s not a fad. People will continue to live indoors no matter what.

Property values are funny things. They continue to rise in almost any environment: war, pandemics, Republican administrations, Democratic administrations, impeachments, killer bees, societal unrest, years the Red Sox win the World Series, almost anything. Why? Because people like living indoors. We are not a society of Bedouin nomads, camping enthusiasts, or Vikings. We like heat, plumbing, running water, and other creature comforts that come with permanent shelter. Property values only have one Achilles heel or kryptonite, and that is a near total financial collapse that results in banks not loaning money.

I’ll say it again: The two times in my life where values cratered were eerily similar: Billions of dollars in bad mortgage loans that caused a plethora of bank failures, resulting in a Stock market crash and a financial crisis where the mortgage industry got overcautious and values declined. In the late 80s, the massive Savings and Loan collapse preceded Black Monday in 1987, and a doozy of a recession that dealt a blow to values that didn’t recover until the early to mid 1990s. In the late 2000s, billions of dollars of subprime mortgages caused the subprime lenders to fail, and the resulting financial crisis hammered real estate more severely than anything since the Great Depression in the 1930s.

I’ll simplify the recipe:

Two scoops of bad paper loans

Bank failures due to bad loans

Financial crisis

Banks curtail lending

Values suffer due to buyers not being able to borrow

People have borrowed money and bought real estate despite wars, crazy rates, pandemics, terrorist attacks, inflation, bad Oscar years, crappy Star Wars sequels, and even New Coke. Why? Because people like living indoors. As a matter of fact, there is absolutely no historical correlation between rates and values. In 1975, the average home value was $38100. Rates that year were in the 9s. In 1981, rates approached 17% and property values nearly doubled from 6 years prior. In 2005, the average property value in the US was 232,000, with rates just under 6%, and in 2010 rates fell nearly a point but values fell to $222,000.

This isn’t to say that rates aren’t a factor. They are. I’ve written about this twice, and used the manipulation of rates to predict, rather accurately, both the crash of 2008 and the spike in values were are seeing today. By the way, I smile at the first old blog post from 2006 because my brother, the financial guru, made the following comment: “the stock market is likely to be in very good shape in 2008.”

I can’t speak to the current stability of the stock market, but I do know that there is a fraction of the amount of risky mortgage paper out there now compared to 2007 or 1986. And that bodes well for the health of property values for the foreseeable future.

Last week saw a posting by a manager at another firm of their agent holding up a commission check, congratulating the agent on their recent closing.

As we used to say back in the 80s, gag me.

Yes, I know we work on commission and closings should be celebrated. But spiking the ball over your compensation is cringeworthy and not edifying the profession. The public knows we are typically paid on commission. It’s no secret. But it’s just gauche to make a closing about the paycheck and not about the happy result for the client.

I’d get ill if the contractor who did my roof a few months ago posted a photo holding up my check for the job. Wouldn’t you? Years ago, I contracted a web provider for a specialized website for a project we were taking on. It wasn’t cheap, and when he thought I was on hold, I heard the guy tell a someone how he “just signed up a mac-daddy” deal. I wasn’t shy about the fact that I heard him, and the way he hemmed and hawed told me that he didn’t mean for me to hear that. No kidding. I had just made a difficult decision on a financial commitment, and his touchdown dance made me second guess my decision. Spoiler alert: I wouldn’t do business with them again.

Commission compensation for some is a touchy subject. My agents are worth every penny they are paid and more, but I’ve never posted a photo of them holding up a check, because that’s not where the emphasis should be. Yes, we are paid, but we are paid by taking care of the clients. THAT is where the focus belongs.

I’ll repeat that: Real Estate commission is tied to serving the clients. We are fiduciaries. We aren’t brain surgeons, but we shepherd the largest transaction of most people’s lives, and we should conduct ourselves to reflect that. You don’t see a surgeon posting a picture of themselves holding up a check and saying “I just removed a huge tumor! Yay me!” Nor would you ever see a CPA doing the same with a caption of how they just completed a massive schedule C for a client. And I’m fairly certain my therapist doesn’t have a pile of my co pays in front of a camera lens for social media either. Their emphasis is on who they serve, not what they get out of it. It should be the same thing with us.

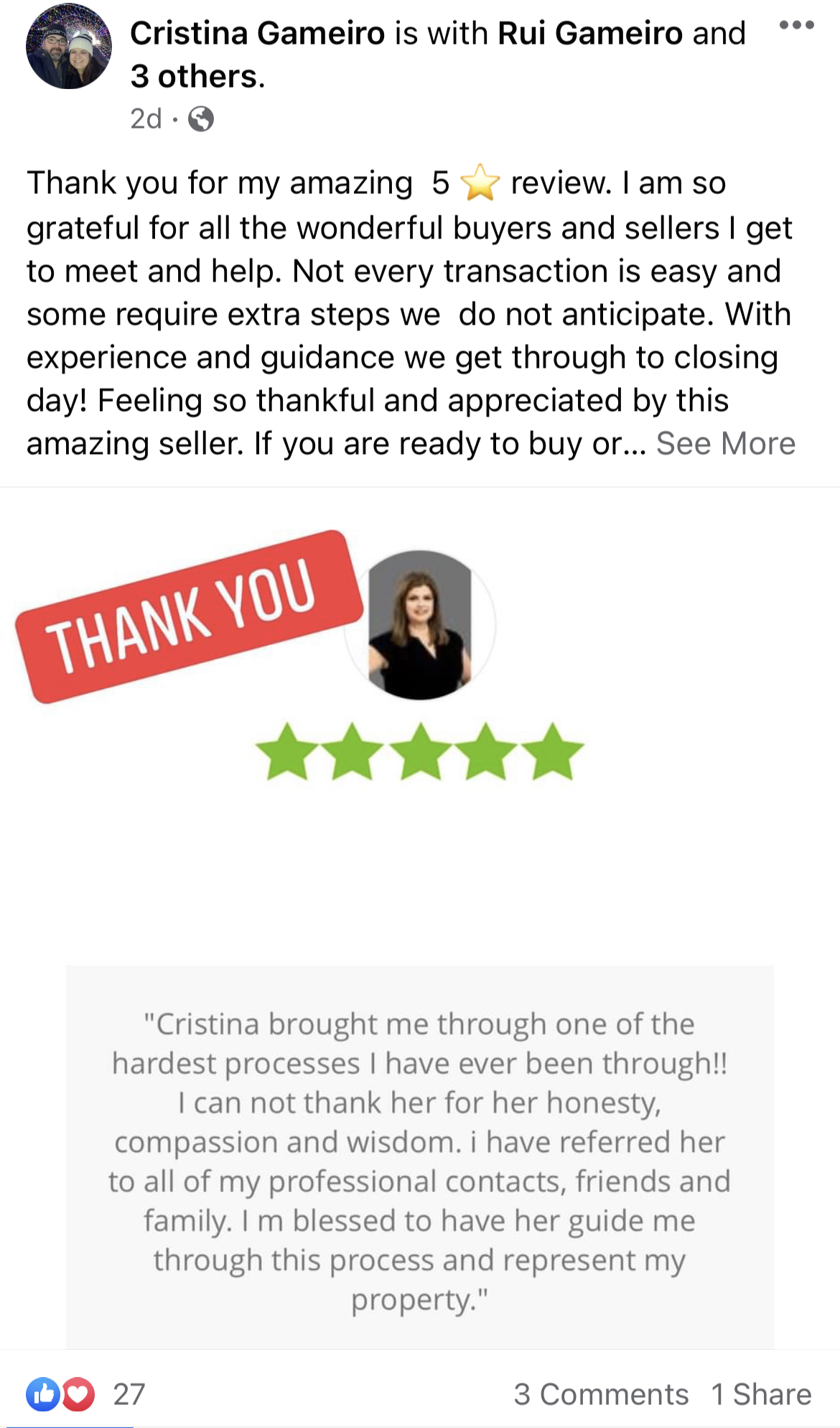

Of course we celebrate closings. But to me the best way to do so is what many of my agents like Cristina Gameiro share: A 5-Star review from their client of their professionalism and performance. That says far more than a check.

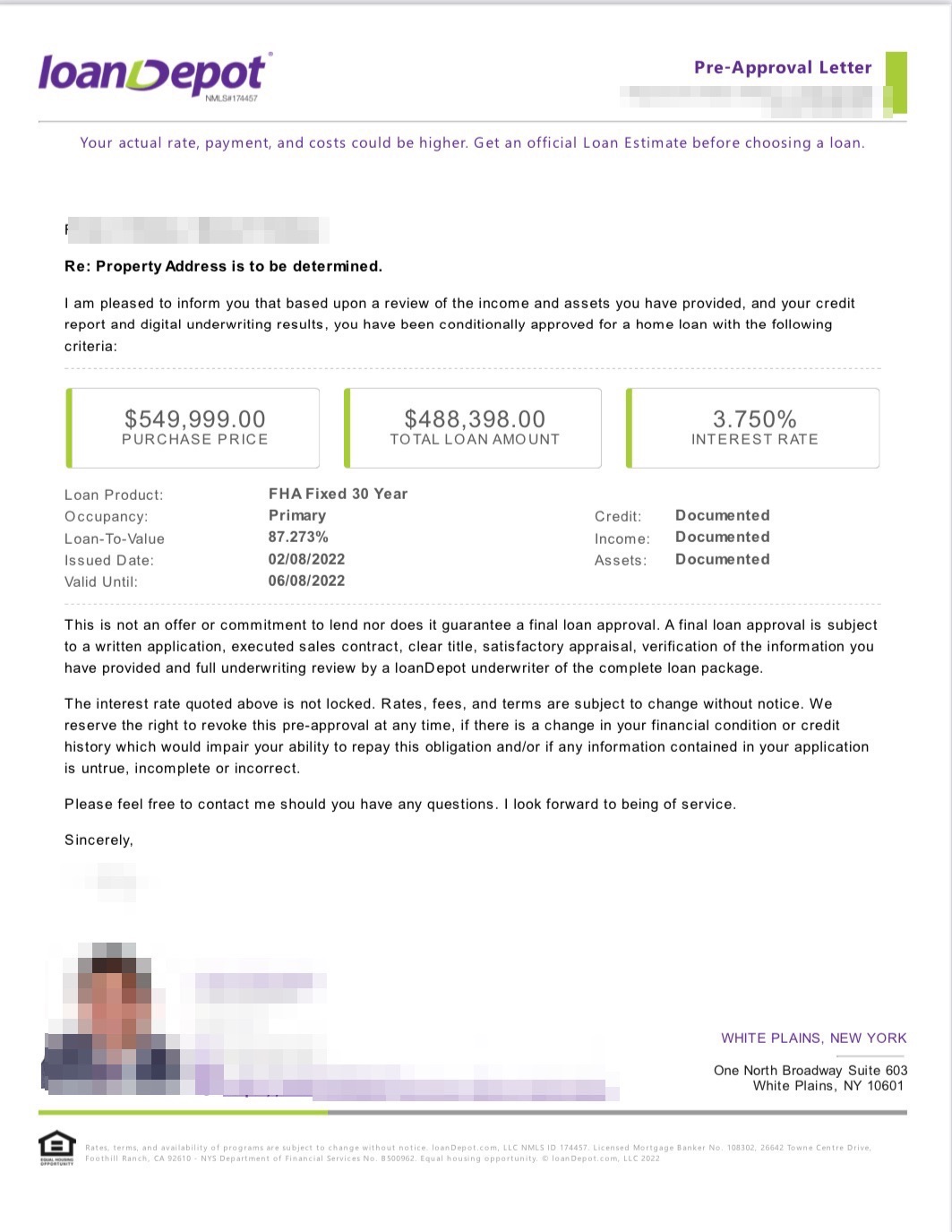

You’ve read it before, unless you just learned to read (in which case house hunting is a long way off for you), on financial platforms, blogs, real estate websites, magazines, newspapers, and maybe even ancient hieroglyphs: get pre approved before you start looking at homes.

This is what you’ve never read from any credible source: sure, go ahead and start calling agents to show you listings before you speak to a lender. Why haven’t you seen it from any legitimate professional? Because it wouldn’t make any sense.

When COVID first hit, the entire industry marshaled the will to finally put their foot down and mandate that no one would tour a home without a pre approval. Consumers complied, and it didn’t even require an explanation because common sense shouldn’t. Showing confirmations didn’t go out without an e-mail with a COVID disclosure and a pre approval. In a huge cloud of Corona virus chaos, this was a silver lining. But as time went by and the pandemic numbers dropped, we got sloppy. People stopped being so cautious. And the small battalion of home seekers without a pre approval swelled into a wave of unvetted, approval free question marks that wanted us to open doors.

So, without further ado, here are more reasons why you should get pre approved first:

You won’t get your heart broken. In this market, listings go fast. If you see it on a Saturday, it’s going to highest and best by Monday. And the winning bid will have their complete act together. You won’t. And damn, you would have been so absolutely happy in that house.

You need to know what you can afford. In a world that rightly demands professionalism from agents, lenders, attorneys and everyone else involved, it’s the common sense, professional thing to do before shopping.

It’s only fair to the seller. When you visit a house for sale, that is someone’s home. They sleep there. They eat there. Children are raised there. And with the rare exception of vacant homes (which have their own rationale fore requiring a pre approval), those people will return there a few hours later to eat, sleep, and live. You are a guest. The seller, their kids, whoever is living there made arrangements to be out of the house to accommodate your visit. The seller has a right to know that the person walking through their children’s bedroom, opening their cabinets and closets, and spending time inside that home is at least qualified to make the purchase.

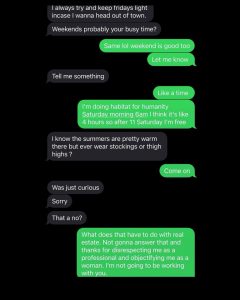

It’s safer. Real estate agents make a living meeting strangers alone in empty houses. When people call us and want to see those properties, virtually anonymously, that is a risk. I know too many agents who have had to deal with creeps, perverts, harassers, deluded suitors, and worse. I am the charter president of the Beverly Carter Foundation. Beverly was kidnapped and murdered by monsters masquerading as potential buyers. I want every single one of my agents to get home safely and with peace of mind, every day. No exceptions. And I don’t want to hear from a seller that something is missing, and not be able to tell them who was in the house. The graphic posted is a real text exchange encountered by a colleague. She’s sadly not alone.

It’s reasonable. When you test drive a $2000 used car, they get your license. If you buy spray paint they check your ID. If you want to buy cigarettes, they check your ID. Yet, if you want to walk through a 6 or 7 figure cost home you can’t possibly think it OK to not have any credential or qualification.

You have to play your part. Lots of people are involved in the sale of a home. Last year, I got a call from someone who said they were a cash buyer who wanted to see a vacant unit in a condo complex where they said they also lived. In checking the listing, it stated that no showings would be approved without proof of funds or a pre approval. She took some sort of offense to this, stated louder that she was a cash buyer, and that she’d provide proof if she was interested after seeing the place. Not only was this backwards, but she was making it all about her. That’s the kiss of death in any market, but in this market, that’s laughable. Sure the place is vacant, but the owner still incurs liability for an unsupervised property. An agent still needs to drive over and accompany the showing. The listing agent still needs to follow up. And the domino effect of their family, colleagues and other clients is no small thing. The value of other peoples’ time should never take a backseat to 5 minutes on your computers and hitting “print.” I’ll die on the hill that this person was curious and wanted a free tour guide to satisfy her inquisitiveness.

It’s absurdly easy. Upon occasion, we will have a prospective buyer tell us that their pre approval is “in process” or coming in a few days.Come on.I do this for a living.It takes 15 minutes to get pre approved unless you are a hot mess. This is the computer age. A few minutes on a call with a loan officer, an email with your last paystub and a bank statement, and you’re due for a shiny fresh pre approval letter within hours.

Some of the concerns we hear about getting pre approved are easily addressed:

No, it will not adversely affect your credit score. Buying a $200 dinner on your credit card will lower your score more than a single mortgage inquiry. You’d need dozens of inquiries to truly damage your credit score, because that would mean you are frantically trying to borrow. One, two or three inquiries from lenders over the course of weeks, or months is virtually meaningless.

As I said above, saying that you don’t want to waste your time getting pre approved unless you find a home you like is utterly selfish and insensitive to the value of the time of all the others involved in accommodating you. The buyer agent, the listing agent, the sellers, the other buyers who can’t see the home while you’re taking the time, the family and co workers of the aforementioned agents who lose time while they are with you, all disrupt their schedule to assuage your curiosity. That’s not cool. You don’t live in a bubble. If you do something that involves the time and help of other people, play your part or stay home.

You’re waiting for XXXX and want to get a head start? By the time XXXX happens this house is gone. So please wait and get your financial house in order.

And yes, dangling that you’ll list your home with us if we just show you this house first is also not cool. Let’s take a look at your house and ascertain that you are a ready willing and able seller first. Let’s not put the cart ahead of the horse.

If you sense an eye roll quality to the tone of my piece here, you aren’t wrong. I originated mortgages for 7 years. I’ve brokered thousands of transactions. I’ve done this every day since the 90s. I oversee close to 100 agents, and the exponential amount of interactions they have with the public in a fast moving industry like this, especially in the current market, boggles the mind. But I’m not writing this for them. Scroll up. I’m also writing this for you. Play your part and invest the 15 minutes in yourself.

While making a training video on market reports for the agents this past week, I clicked on an oldmarket report I wrote in November 2011for Ossining. Among other things, I noted that there were 119 single family homes available for sale in the school district at that time. In working on current data, I had to blink and see if the current inventory number was accurate, because it is cartoonishly low.

12.

There are 12 active single family homes in the Ossining School district, and that is at a time when the spring market inventory should be trending up. This has affected prices significantly- in November 2011, the median price was roughly $380,000. Today? $504,000. That’s almost a 33% increase.

Contributing to the low inventory is the reticence of those in a position to sell because they don’t see a viable housing option currently listed. That’s scary. My advice for prospective sellers who aren’t sure where they’ll go if they sell: Look at your options- sell subject to finding suitable property, make sure you have a flexible, extendable closing date, and, if you can, buy before you sell.

Buyers need to have their act together- make sure you have a pre approval for the house you want to see Sunday, because it will be gone by Monday to someone who already learned that lesson the hard way. Buyers in the market need to be locked, loaded and ready to go. The competition for such a small amount of options has never been tighter.

Writing the year’s wrap up used to be my New Years eve ritual, but with the scale of the job these days it’s impossible to quantify everything by midnight on 12/31. So let’s dive into my happy summary of a great year for the brand on the first business day of the new year.

The Numbers

2021 was by far the most cartoonish, crazy year I have witnessed in the industry, going back to 1996. Buyers were in the stiffest competition I’ve ever seen, and sellers were in the driver seat by a gigantic margin. This made life for listing agents comparatively advantageous (although nothing in this industry is truly easy), and for buyer agents it was trench warfare. I smile when people tell me that I must “have it easy” in this hot market, as they don’t know that the lack of balance complicates things enormously for all buyers, and no transaction can occur without a buyer. That difficult side of the puzzle notwithstanding, 2021 was the best year for J. Philip Real Estate by most conventional metrics.

Overall, the brand closed on over $150 million in volume for the first time in history. Last year we eked past $140 million but this year we were at $156 million, an increase of over 10%. We remain the top selling Westchester and Putnam county based independent brokerage for another year.

34 of our associates closed $1 million or more for the year, the highest total in the firm’s history. This means more to me than market rankings, because when someone entrusts their livelihood to us, we want them to be able to be a primary bread winner if they choose. One of my happiest stats is the sheer number of our professionals who are at that level of production. We have them by the dozen, and for a firm our size that is something we are fiercely proud of.

Another stat I pay close attention to is the amount of property we put under contract each week. Happily, we torched 2020 by nearly 11%, with close to $160 million put under contract, and that has us going into 2022 with good momentum.

We haven’t had our awards event yet, so I cannot make a shout out to recipients, but I can say confidently that this year’s list will dwarf that of prior years.

Accolades

Where to start? Chief Operating Officer Jenn Maher was an absolute superhero in 2021, instituting systems and architecture that epitomized the best practices of working on one’s business rather than just in it. The firm’s policies and procedures were revamped and updated, the managerial and administrative structure was rebuilt, streamlined and expanded, the Inside Sales Division was started, transaction management was expanded, and overall I can look you in the eye and say that if 300 new agents walked into the door tomorrow, we could onboard, train and deploy them as smoothly as if half a dozen did. Among other initiatives Jenn spearheaded was the adoption of an entire planning and accountability system used by the company leadership, the administrative staff, and all of the departments that support the sales force. We now have a crystalized 1, 3, and 5 year plan with clear objectives and the roadmap to make it happen. I’ll happily restate that $1 billion in annual sales has never been more attainable for us thanks to Jenn’s fine work.

Jenn was also a prolific producer of video content, with her “Success in Real Estate” broadcast developing a bigger following, and added to that was our joint “Real Estate Unscripted” broadcast every Monday. Providing licensees and public alike good informative content and commentary has been one of the best ways I have found to build the brand. This endeavor will grow into something special; mark my words on that.

Uber administrative renaissance woman Ronnie DeMeo was elevated to Chief Administrative Officer (CAO), and now oversees several large departments in the back office, as well as remaining my right had and the spiritual leader of the “Core Team” as Jenn terms them, the employee support staff that does admin, communications, sales support, and marketing. This past month the entire admin and management team met to plan the relaunch of the company systems, and I’ve never been in a room with so many smart, talented employees working together to forward the company’s vision. It was a sight to behold.

Josie Faranda stepped up significantly in 2021 as well, helping to tackle the firm’s enormous tech machine, as well as overseeing the fledgling Inside Sales (ISA) department, which is tethered to the aforementioned tech. Josie is quickly taking a complicated digital matrix and helping the personnel run it like a well oiled machine. The entire journey of the consumer from a raw inquiry for more information, to choosing a J Philip agent, through the closing has a cadence and written process that guides our training, agent support, and oversight.

Transaction Coordinator Michele Kantrowitz is among many smart, talented people who have stepped up and helped move our systems forward. Supporting the team in something as sensitive as shepherding the steps to closing a contract is something she does well, and the agents get enormous value from her contribution.

Other steps forward included:

The addition of a virtual CFO to oversee and manage the company finances

The start of the full renovation of two offices

A structured recruiting system with a budget to increase the size of our sales force

The adoption of a new CRM software that “sees around corners” thanks to artificial intelligence and predictive analytic programs

An equally high powered transaction management platform

Establishment of basic Boot Camp Training for new and experienced agents alike

A full compendium of both basic and advanced company training in our Trainual platform, thanks in large part to Lorei Kwok

The new Agent Leadership and Culture Committee with a more clearly defined purpose

Establishment of a Mentor Program for newer agents

A company lead program open to all agents, with the support of the aforementioned ISA program and Transaction Coordinator.

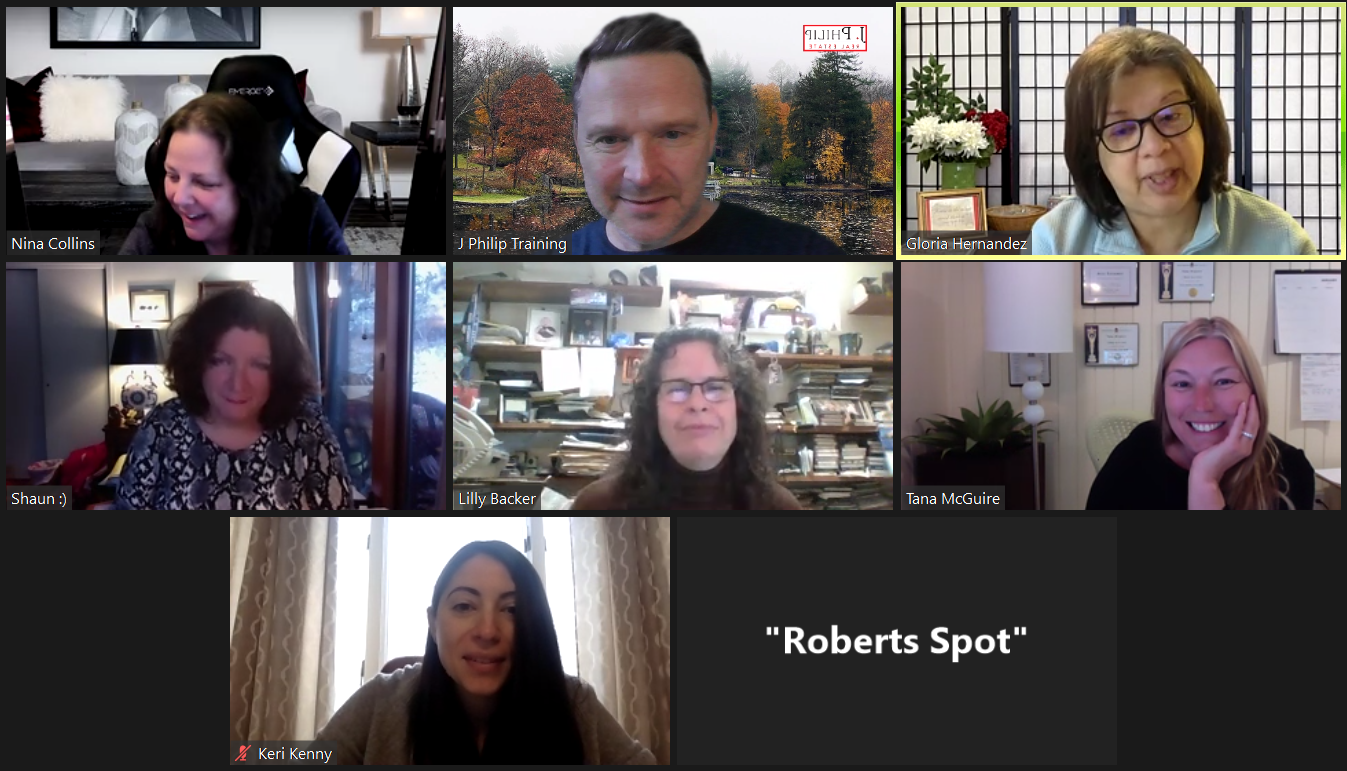

The elevation of Keri Kenny to Commercial Director

I am so humbled that this team of sharp, committed professionals has chosen this brand to share their talent. There are so many awesome people contributing it’s impossible to name them all. Many thanks to Brittany Alvarez for her great training contributions (and a big congrats on the new baby!), to Cristina Gameiro for her tenacious work and support in building out our team model, and so many others who rolled with the changes both inside the brand and out there in this industry.

Coming attractions

I announced at the end of last year’s wrap up that we’d roll out a new company website and expand the size of the brand. The new website went live in the first quarter, but I was not satisfied with it, so expect a better version of jphilip.com this winter.

We are working on expansion, and have hired a consultant to spearhead something special. Stay tuned there.

We see the future of the top producing agent significantly tethered to the team concept, which is essentially like a brokerage within the brokerage. Few traditional brands will admit this, but they aren’t excited about that idea. Teams are not as profitable as individual agents are to brokerages, but our plan is to scale the brand so that teams will be welcome, will flourish in our model, and the arrangement will be a win/win for all parties. I’ll restate it more clearly: J Philip Real Estate is enthusiastically a team-centric brokerage. Expect bigger and better teams growing with us.

Me, Myself, and I

Personally, I served my first year as a director of the Hudson Gateway Association of Realtors; I had been on the board of the MLS for a decade and served as president in 2014, but this was my first time on the association side of the organization. I also served another year on the board of the Beverly Carter Foundation, an organization committed to agent safety on the job. Locally, I was on the Ossining Historic Preservation Commission, and on the Committee for the establishment of the Sing Sing Prison Museum. My kids are healthy and doing well, I’m in a great relationship for close to 3 years now, and I wake up every morning feeling blessed and grateful.

The Wrap

I take no small amount of joy in observing that 2021 wasn’t just our highest production year, it was the year we built a bigger plane as we flew it. The absolutely gigantic projects we took on -simultaneously- certainly turned the agents’ collective heads as if we were crazy. To their credit, they hung in there, were supportive and comported themselves like the true professionals they are while we challenged them with so many changes. These are the people who make me feel confident in promising that before the next 5 years is over that J Philip Real Estate will be at over a billion dollars in annual closings. I love this bunch.

I can’t post a photo of all the awesome agents, but here is the team supporting them like nothing I’ve ever witnessed.

I recently closed on this listing for over $50,000 over asking price. This is an example of how values have grown in the area. The description of the home in the MLS is as follows:

“This is the village of Briarcliff Manor lifestyle you’ve sought in a 5 bedroom split that lives like a colonial. Master suite was an addition so you get 2 bedrooms with baths en suite. Balcony overlooking back yard will reveal a marvelous rear garden, a patio with custom masonry including a working stone oven & seasonal foliage to die for. Rectangular corner lot leverages the quiet tree lined neighborhood with ample room for recreation, gardening & entertaining. Two car garage plus parking for 6-8 cars easily. Inside you’ll fall in love with the spacious kitchen with garden views, living room with high ceiling & custom wood burning fireplace, dining room with doors to the back yard, and a family room on the lower level lots of light, access to the patio, and a half bath for convenience. Law Park with its fabulous pool and downtown are moments away by car. All bedrooms are roomy and boast ample closet space. Gas backup generator. Pride of decades long ownership shines through here!”

This one is sold, but we have more. You can call me at 914-450-8883 for more information.

We were actually gratified to list and sell this property after selling it to the owners a few years prior. They did benefit from appreciation, selling for $568,000 after purchasing it for $395,000 7 years before.

As described in the MLS:

This is a adorable 3 bedroom, 2 bath ranch home on nearly half an acre with a garage and double sized driveway. It has excellent flow, a chef’s kitchen and fabulous outdoor deck overlooking picturesque garden and yard. There is a custom built shed for all your tools and hobbies. Established perennial bed, and garden has been organic for the last 7 years. Many new upgrades including Burnham boiler in 2014 and improved insulation in 2014 after NYS energy survey. New kitchen appliance in 2018, a 6 burner range, dishwasher, and a high volume Zephyr Air Extractor over the range for excellent exhaust. Second refrigerator in basement. It has a fireplace in the family room and an upgraded electrical panel 2019.

While the house is nearly 1500 square feet, the full basement offers additional space.

This marks the first time I have not posted this update on New year’s eve, so it feels weird to wrote a piece about 2020 in February 2021. However, I’ve got great reasons.

2020 was by far the most surreal year of most of our lives. When the pandemic restrictions began in March, one had to wonder if the new normal would become an extinction event for the brand. There were more sleepless nights than I can recall since the real estate crash in 2008. It was a rough matter from every angle; society was in an upheaval, everyone was concerned about their own health and that of their loved ones, regular life events were disrupted and altered, and a dark cloud of uncertainty seemed permanently above our heads. What added to the difficulty was the fact that we started out in January and February at a red hot, record-breaking pace. Then, just like that with the flip of the news cycle switch, we were looking at months of possibly no or a pittance of revenue.

That’s the backdrop. Q1 wasn’t even over and the possibility of the industry, and my brand, being dead in the water, loomed large. I founded this firm in 2005. It is my life’s work. I don’t think I can do justice describing that feeling of foreboding.

But a funny thing happened. We learned we were built for this. All of the online training, remote meetings, virtual reality imaging and other tech that we have invested in over the years was already in place, ready for us to implement rigorously. And implement we did.

As soon as the lockdowns began, we began an intensive schedule of remote events. Some were fireside chats. Some were happy hours. Much of it was intensive training on how to pivot and adapt. With rare exception, we were in better communication with our agents than we had before in the age of in person meetings and the odd phone call. The results in March, April and May were sub par for the spring, but not awful. When restrictions were partially relaxed in June, the dam broke. Executed contracts in June were 38% higher than the prior June. Contracts in July were 89% higher than July 2019. It continued. Year over year, we had months that exceeded prior totals by 34%. 88%. 128%. 53%. When all was said and done, 2020 saw close to $150 million worth of property put under contract, $40 million better than our prior best year of 2019.

The brand closed $141,500,000, better than 2019’s prior high by 34%. 383 closed transactions blew the doors off prior best totals.

Did webenefit from the exodus of New York City dwellers to the suburbs? Yes. But it’s never that simple. Inventory was historically low. Many buyers lost income. The competition for listings was intense, with buyers offering on 5 and 6 homes before they got a yes. Many brands were down from 2019. We were up by over a third. In the frenzy of low inventory and too many buyers competing, not everyone can come out winning. More often than not, our clients prevailed. Nothing punctuated the need for a good agent like 2020 did.

Other good news:

In July, Jennifer Maher wasnamed Chief Operating Officerof the firm. Jenn’s stepping up in the pandemic, to say nothing of her contributions to the brand since joining us in 2013, made this inevitable. Jenn also got married in December. Some people thrive in adversity. If you’re in a foxhole, you want her with you. She is now a partner in the company, operating principal of J. Philip Commercial Group, and COO. Not bad.

The firm cracked the top 20 of companies in our market for units sold. Out of close to 1400 companies that operate in our primary 5 counties, we ranked 19th overall, and were the top-selling Westchester/Putnam based independent. In Westchester Alone, we were 17th. in Putnam, we were top 5.

Brittany Alvarez

The firm named a newAgent Leadership Council, with Tana McGuire, Kisha Ocasio-Riviezzo, and Verona Cruz filling important roles as liaisons between leadership and the agents.

Congratulations go out to Brittany Alvarez, associate broker, former Rookie of the Year and Person of the Year, for adding Top Producer to her accolades. Between New York and Connecticut, Brittany closed over 40 sides worth over $14 million in 2020.

Gloria Hernandez

Congratulations to Gloria Hernandez for being named Person of the Year for 2020 for her teamwork, leadership, and contributions to the brand in an unforgettable year. Gloria will be retired from management later this year but will remain with the brand as an associate broker. We are fortunate to have her.

Personally, I wrapped up 9 years on Zillow’s Agent Advisory Board as well as a director role with the Hudson Gateway MLS and I was elected to serve as a director for the Hudson Gateway Association of Realtors.

It is a peculiar feeling to write about the company’s best year in the backdrop of such societal upheaval. I have to express a deep pride in the team for their stepping up. The culture here is difficult to truly render, but it inspires me. When the pandemic first began and revenue was uncertain, a number of agents offered to defer portions of their commissions to ensure the company had the cash flow to operate optimally. That is humbling. As I look back on a year that exceeded profit expectations, I am deeply grateful for their care and ownership of their brand.

Looking forward to 2021, while I hope and pray for society to return to normalcy and relative safety, I am working on bigger things for the company:

A significant expansion of the brand size and market share

A brand new company website

A state of the art back office tech suite which will empower the agents to do an even better job than before.

And that, dear reader, is why I couldn’t post the good news sooner. There was more to gather than ever.

$575,000 buys an awfully nice home these days, like the 3 bedroom, 2 bath split we recently closed for a seller client on Leawood Drive.

As the MLS described:

This is a TRUE GEM in a four cul-de-sac neighborhood of about 70 houses! Besides being completely renovated and move-in ready, what sets this house apart is its property; with nearly twice as much land as many plots, the owner really does have the “park-like” setting you read about! With woods on one side and in back, and location in the cul-de-sac – it also is quiet and has much more privacy, too! Back to the house itself, the floor plan on the main level features an updated, Eat In Kitchen with a formal Dining Room and doors out to a HUGE Deck – perfect for entertaining. Upstairs, the three very nice-sized Bedrooms feature pristine hardwood floors – much of them recently refinished – with both the Master Bedroom and Hall having beautifully modernized, sleek and polished bathrooms. Downstairs, there is a newly painted, large Laundry Room, and a HUGE carpeted Family Room/Office or fourth Bedroom with a door out to the side yard.

This one is gone, but we have more. Call me at 914-450-8883 and my team can help you find your best new nest.

I’m so glad you asked! If your budget is in the low 500’s, you might like a home like the one we just closed on Avis Court, a 3 bedroom 2 bath split on nearly 3/4 of an acre on a cul de sac. The final sale price was $513,500. Best of luck to my seller, a good human being and a friend.

As described in the MLS:

Move in condition front/rear split on a plum 3/4 acre cul-de-sac lot. Open concept in living area, with vaulted ceiling in the living room, faux mantel, and formal dining room off the kitchen. Appealing deck overlooks the spacious rear yard. You’ll love the view out of the wood Andersen windows. Lots of parking and 1 car attached garage. Front level has a family room and office, although there are possibilities for a media room or guest quarters. Good sized bedrooms on the upper level with ample storage base, and then you have the basement with storage that runs the length of the house. Pride of ownership shows throughout, and the location and setting are unbeatable!

This one is sold but my team can help you find one of your own- call 914-450-8883 for more information.

If your budget is $625,000 you might be able to buy a home like the raised ranch we recently closed on Country Club Lane with a Hudson River View.

As described in the MLS:

Your opportunity to own a home with breathtaking year-round views of the majestic Hudson from the living room, dining room, master suite, deck and enclosed porch alike. An amazing lifestyle awaits you on this cul-de-sac location with a gorgeous half acre, inground pool, enormous patio, rolling lawn, and much more. Boasts a large eat in kitchen, a massive rec area with fireplace downstairs, 2 car garage, and enormous potential for your updates and touches. Tremendously convenient location to commuter points, recreation, shopping, parks and the splendor of the Rockefeller preserve all a stone’s throw away.

This 4 bedroom 3 bath home needed some work, but we can find you something that fits your needs if you connect with us. Call 914-450-8883 to get the ball rolling!

$560,000 will buy you a mighty nice 3 bedroom 3 bath split on a dead end like the one we closed on last month.

As described in the MLS:

This wonderful, pristine house on a quiet cul-de-sac is ready for you to move right in! With a three-season Sunroom and HUGE basement area to make your own NOT included in the square footage, this house truly lives like a much larger home than many in the desired neighborhood. The updated Kitchen with stainless steel, GE Profile appliances COULD be converted to be Eat-In – OR use the current large counter areas and cabinets to cook and entertain to your hearts’ content! The main level is light and bright with a nice flow throughout, and has access from that Sunroom down to an expansive patio and wonderful yard. The Family Room downstairs is large – over 250 square feet – and has a door out to the side yard for your convenience, or if you want the flexibility of an office or even guest room. Finally, the separate Laundry Room and Full Bath downstairs make for SO many possibilities!

Connect with me at 914-450-8883 and my team will help you find you next dream home!

(Note: the following piece was originally published in Inman News)

Like many of my colleagues, I’ve been reading — with great concern — about how the ripple effect of the coronavirus pandemic is playing out and how it will affect my business.

However, unlike many of my colleagues across the nation, I am seeing serious consequences in my own backyard. New York state ranks second behind Washington state for coronavirus cases. As I type this, my market of Westchester County accounts for over half of the documented COVID-19 cases in New York (178 at last count).

Only a few miles from one of my offices in New Rochelle, New York, there’s a 1-mile diameter containment zone. The governor brought in the National Guard to assist in cleaning up houses of worship and schools, which will remain closed for two weeks.

Schools are closing like we’re under 6 feet of snow. There’s no widespread panic, but there’s certainly grave concern.

Having lived through the Great Recession, I’m really not in the mood for another disruption. Although, even if things get demonstrably worse, it will, in all likelihood, never be a full-blown crash like the one we saw in 2008.

That said, with so many events being cancelled or postponed, a disruption is inevitable. So what can we, as an industry, do to minimize the detriment and squeeze results out of the scarcity of an alarmed consumer base?

For markets where showings are still happening, advise your clients not to bring their young children or aging parents along on home tours

Those over 60 are most susceptible, and this practice would minimize their exposure to contagions. It also provides the added fringe benefit of not having a front-row seat to grandma’s sticker shock when she finds out how prices and taxes have gone up since she last bought a house in 1988.

Associations: Please, for the love of God, stop calling meetings

Last week, I got an invitation to a broker-manager meeting my association is holding on March 18. To its credit, the association allowed remote access as news changed.

Since my business partner just became a grandmother last week, she shouldn’t be forced to miss an important meeting because she wants to hold her infant granddaughter. Allow us to attend remotely. The technology isn’t new. Come on associations, we can pivot.

Support local businesses

It might be easier to shop on Amazon, but they will never refer you business. That Chinese restaurant down the road is likely taking it on the chin, especially with so many states and counties placing limits on large gatherings and bars and restaurants.

Be a mensch, and have lunch there if you can, or buy a gift card if they cannot serve. Grab a loaf of bread and chicken soup at the corner deli. Now is a great time to get acquainted with local cleaning operations. When all this blows over, they — and all of their referral sources — will know you were a stand-up supporter. That will make you money.

Invest in 3D imaging and virtual reality

Even if folks aren’t going to actively tour homes, you can bet that they are looking online. 3D tours are a phenomenal differentiation, as well as a great way to attract more inquiries once things return to normal. We see open houses being cancelled in many markets, and this can help.

Brokers and managers — go virtual

Chill out on the office meetings, and start leveraging platforms like Zoom, GoToMeeting and Google Hangouts (that goes for you too, associations).

Keep your personal space

If you’re in a market where it’s customary to drive clients around in your car, rethink the practice. This is a rarity in liability-conscious, litigious New York, but I do know it occurs more frequently elsewhere. Now is no time to be in such close quarters with people you may not know very well.

Be consistent

Whatever business practice changes you make, apply them consistently. NAR released guidelines that aren’t earth-shattering, but they are useful. One of the more timely takeaways for me was that if you’re going to make changes for one client or customer and not the other, you could run afoul of fair housing guidelines. It’s common sense — but crucial.

The situation sucks. It really does. I see a hot start for my own company hijacked by the pandemic, and I see my industry brethren arguing over politics and health policy.

But we will get through it, and when we do, we should hit the ground running with the pent-up demand. Remember: People prefer to live indoors. There will be plenty of work to do when this passes, but we can produce results in the interim as well.

If you like a 3 bedroom, 2 bath Tudor styled cape on a landscaped lot with a detached 2 car garage, this was the place that we closed on last week.

The MLS description:

Tudor-inspired Cape with oversized yard & a fantastic two car detached garage with loft on a quiet street near everything. Solar energy! Brick & stone pre-war home with tons of upgrades without losing the traditional soul of the period. Double-sized lot currently loved with gardens, ample greenery with plenty of lawn & still room for parking 5-6 cars without the garage. Private rear paver patio, great for entertaining or relaxing. Inside you’ll be inspired by the modern kitchen, well-maintained wood trim and appointments, bright living room with wood burning fireplace, dining room, upgraded bath and two good-sized bedrooms. Upstairs is a renovated master suite with modern bathroom & a walk-in closet/attic area to store enough for a small army. Finished basement rec area (not in square footage). Dynamite location, minutes to the North White Plains metro-North station, shopping, and highways. An unmatched lifestyle at this price point offering modern convenience and traditional charm.

Best of luck to my clients who are flying NORTH, not south, and starting their new life upstate! This one is gone, but I can help you find one of your own! (914) 450-888

Spoiler alert: Best year ever by every metric we employ.

Last year’s summary was wrapped up thusly:

In years past, I’ve made numerical predictions, but this year I’m going to be a bit more coy. I’m looking for good agents who want to grow their practices the right way. My role is evolving from chasing deals to procuring the best training, tools and professional infrastructure. 2019 will be centered on providing those agents with the best tools and training possible, and this year I can say that we’ve never laid the groundwork the way we have in the past 12 months. So I’m not worried about numbers; we’ll let the bean counters do their work while we do ours.

While I haven’t finished the counting, what has been tabulated puts us back into explosive growth. The firm eclipsed $100 million in closed business in our main market area alone before December even hit, and as we grow it becomes virtually impossible to have everything counted by New Year’s Eve. That is a wonderful “problem.”

2019 has been replete with happy milestones:

Our number of closed transactions is up to at least 320 at last count, up 12% over 2018

Our closed volume is now at $115 million, up 15% over 2018

Median sales price is up 9%, when the market itself overall is flat.

Contracts executed for 2019 are up enormously, 15.5%, with a median price 15% higher. This is huge because it means we go into 2020 with momentum and a swollen pipeline of pending business for the new year.

For the 3rd year in a row, our listings sold on average over two weeks sooner than the MLS average, and for a admirable percentage of asking (many selling well over asking).

Happily, for the 4th year in a row, J. Philip Real Estate is the top selling Westchester and Putnam-based true independent brokerage for transactions. No other independent outsells us in those counties. We outpace the market in most categories by 10% or more.

Another accomplishment of note is our inaugural 2019 membership as the exclusive Westchester and Putnam affiliate for Leverage Global Partners, the premier network of independent brokerages. We remain happy members of Westchester Real Estate Inc., the local area’s premier consortium of independents, as well as my continued membership as a Hudson Gateway MLS board member, Zillow’s Premier Agent Advisory Board, and as immediate past president of the Beverly Carter Foundation.

Double digit growth is both exciting and humbling. As the firm has grown, I have had to expand my own knowledge base also, evolving from prospecting and deal making to understanding how to deal with vendors, how to train agents effectively, what resources work and which ones aren’t for us, and a host of other things that weren’t in my original skill set when I started the firm 14 years ago.

Suffice to say, huge debts of gratitude are owed to Jenn Maher, my business partner and friend, Gloria Hernandez, who manages two of our three offices and is a tireless trainer and respected voice of wisdom, and Maureen Jacobson, who for my money is the area’s best business coach by far. In addition to the administrative superteam of Ronnie DeMeo, Rose D’Angelo, Rosaline Cruz and Michele Kantrowitz, we also added my niece Josie Faranda to the tech team. I’ll add a special thank you to Elena Kupka, who stepped up this past summer with advice that made a huge contribution to me both in and out of work.

As we look to 2020, I’ll demur on predictions, but will state that I remain committed to double digit growth in becoming a billion dollar enterprise. We will do it the right way, with solid professionals with whom I am proud to associate. To that end I will continue to provide the best possible tools to the agents, the best available training, and responsive and mindful mentoring. Our agents will have a brand to represent they can be proud of beyond mere numbers. If you are an agent (or considering becoming one) who is curious as to how you can have double digit growth as well, call me at 914.450.8883 and we’ll talk.

I am linking to a short video I posted on LinkedIn recently that acknowledged the firm’s milestone in exceeding $100,000,000 worth of real estate sold in our “home field” MLS for the first time in our history. The MLS scene here is very fragmented, and we belong to several systems (7 to be exact, all within a half hour drive save one), but the one we do the most business on is the Hudson Gateway MLS, which comprises Westchester, Putnam, Rockland, Orange, Sullivan, and several surrounding counties. We’ve done $100 million total before combined among all the systems, but never in HGMLS alone. Not only did we do that, we accomplished it with more than a month left to go in the year.

Overall, the firm is up from last year 15% is number of closed transactions, 23% is closed dollar volume, and a whopping improvement in contracts written year to date: 27% higher in dollar volume than 2018. The contracts are the best metric of the firm’s current deal pipeline and future health.

The market itself is up just over 2% in dollars sold and virtually a dead heat in transactions. We are outpacing the market by well over 20%. This is a wonderful accomplishment for the team, and highlights why J. Philip is the top-selling true independent brokerage in Westchester-Putnam.

In one corner, we have the Hudson Gateway MLS- weighing in at over 1300 firms, 1650 offices, and 13,000 agents.

In the other corner, we have J. Philip Real Estate, weighing in at about 80 active residential agents and 2 Westchester offices, with a 3rd in Putnam.

Comparing the first half of 2018 to that of 2019, HGMLS sold 4.4% fewer single family homes at a median price of .09% less than 2018.

J. Philip Real Estate sales were up 16% in units and at a median price of 18.8% higher than 2018.

The numbers don’t lie. Our team is outpacing the Westchester market by a significant margin.

There’s a reason why this organization is the top-selling Westchester and Putnam based true independent brokerage, and you should contact us to learn the difference for yourself.

My son’s sketch of a home we recently sold in Ossining

It might seem contradictory to say there are two distinct markets in the same geographical footprint, but what we’re seeing in Westchester and the surrounding counties is in fact two entirely different markets. I know that there are tons of market reports out this time of year (the beginning of Q2, that is), but I’ll summarize thusly:

Starter homes are overheated due to low inventory

High end is softer than pizza dough

To be clear, starter homes have always had a faster absorption rate than more expensive properties due to supply and demand, but when tax policy and low inventory collide, the markets have become caricatures of themselves.

Why are more affordable homes in such short supply? I have several reasons.

First, we are reaping what we sowed when rates were manipulated by the government years ago to stimulate a sluggish market. Folks who refinanced 5-7 years ago at 3% aren’t too excited to pay that off and buy another home at 5%. So, the people who might otherwise sell -especially empty nesters- are holding on longer and dealing with mowing lawns another year or two to milk that low rate a little more.

Second, there’s always a lag with consumers being savvy to the the actual market conditions. We saw it in 2008 and 2009 when sellers couldn’t get their minds around the fact that it was now a severe buyer’s market. Then again in 2013-14, buyers were often caught flat footed to discover that after 5 years of having sellers over a barrel, they actually had competition to purchase a home they liked.

There are other reasons too (a significant shadow inventory no one wants to talk about being one), those two facts alone are significant.

Why are higher cost and luxury homes not selling?

Tax policy has put that sector into a tailspin. In Westchester, where million dollar homes are relatively commonplace, tax laws have changed to neuter the advantages that once came with the mortgage interest deduction and the ability to write off property taxes. For a home that costs $1.1 million for example, the purchaser has to pay an absurd “mansion tax,” has a lower amount of interest they can deduct, and their property tax deduction is capped at $10,000. That has created a “wait and see” attitude among would-be purchasers, inventory has piled up and gotten stale, and the dynamic is the exact opposite of starter homes- it is in fact very much a buyer’s market in most (not all) places.

So, if you’re selling a starter or affordable home, it’s the best of times. If selling a more expensive property, it’s the worst of times.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

I got a question from a client about the effect that installing solar panels might have on their home’s value. It’s a good question, actually. Years ago when hurricanes knocked out power in our area for more than a week, I opined that backup generators would become the new status symbol. While I wasn’t wrong, green initiatives are gaining momentum and NAR even has a Green Housing certification for agents.

I got a question from a client about the effect that installing solar panels might have on their home’s value. It’s a good question, actually. Years ago when hurricanes knocked out power in our area for more than a week, I opined that backup generators would become the new status symbol. While I wasn’t wrong, green initiatives are gaining momentum and NAR even has a Green Housing certification for agents.

I’m relatively old. I remember Nixon resigning office, Tang commercials, news stories on the war in Vietnam, and lots of other things from when Kitchens were green and gold. I remember when mortgage interest rates topped 20% in the early 1980s, and my father telling my mother how rates didn’t matter, payment amounts did. He was an accountant, so he wasn’t playing out of position on that one.

I’m relatively old. I remember Nixon resigning office, Tang commercials, news stories on the war in Vietnam, and lots of other things from when Kitchens were green and gold. I remember when mortgage interest rates topped 20% in the early 1980s, and my father telling my mother how rates didn’t matter, payment amounts did. He was an accountant, so he wasn’t playing out of position on that one.

I’d get ill if the contractor who did my roof a few months ago posted a photo holding up my check for the job. Wouldn’t you?

I’d get ill if the contractor who did my roof a few months ago posted a photo holding up my check for the job. Wouldn’t you?

You’ve read it before, unless you just learned to read (in which case house hunting is a long way off for you), on financial platforms, blogs, real estate websites, magazines, newspapers, and maybe even ancient hieroglyphs: get pre approved before you start looking at homes.

You’ve read it before, unless you just learned to read (in which case house hunting is a long way off for you), on financial platforms, blogs, real estate websites, magazines, newspapers, and maybe even ancient hieroglyphs: get pre approved before you start looking at homes. It’s safer. Real estate agents

It’s safer. Real estate agents

I recently closed on this listing for over $50,000 over asking price. This is an example of how values have grown in the area. The description of the home in the MLS is as follows:

I recently closed on this listing for over $50,000 over asking price. This is an example of how values have grown in the area. The description of the home in the MLS is as follows:

We were actually gratified to list and sell this property after selling it to the owners a few years prior. They did benefit from appreciation, selling for $568,000 after purchasing it for $395,000 7 years before.

We were actually gratified to list and sell this property after selling it to the owners a few years prior. They did benefit from appreciation, selling for $568,000 after purchasing it for $395,000 7 years before.

$575,000 buys an awfully nice home these days, like the 3 bedroom, 2 bath split we recently closed for a seller client on Leawood Drive.

$575,000 buys an awfully nice home these days, like the 3 bedroom, 2 bath split we recently closed for a seller client on Leawood Drive.

If your budget is $625,000 you might be able to buy a home like the raised ranch we recently closed on Country Club Lane with a Hudson River View.

If your budget is $625,000 you might be able to buy a home like the raised ranch we recently closed on Country Club Lane with a Hudson River View.

$560,000 will buy you a mighty nice 3 bedroom 3 bath split on a dead end like the one we closed on last month.

$560,000 will buy you a mighty nice 3 bedroom 3 bath split on a dead end like the one we closed on last month.

I am linking to a short video I posted on LinkedIn recently that acknowledged the firm’s milestone in exceeding $100,000,000 worth of real estate sold in our “home field” MLS for the first time in our history. The MLS scene here is very fragmented, and we belong to several systems (7 to be exact, all within a half hour drive save one), but the one we do the most business on is the Hudson Gateway MLS, which comprises Westchester, Putnam, Rockland, Orange, Sullivan, and several surrounding counties. We’ve done $100 million total before combined among all the systems, but never in HGMLS alone. Not only did we do that, we accomplished it with more than a month left to go in the year.

I am linking to a short video I posted on LinkedIn recently that acknowledged the firm’s milestone in exceeding $100,000,000 worth of real estate sold in our “home field” MLS for the first time in our history. The MLS scene here is very fragmented, and we belong to several systems (7 to be exact, all within a half hour drive save one), but the one we do the most business on is the Hudson Gateway MLS, which comprises Westchester, Putnam, Rockland, Orange, Sullivan, and several surrounding counties. We’ve done $100 million total before combined among all the systems, but never in HGMLS alone. Not only did we do that, we accomplished it with more than a month left to go in the year.

In one corner, we have the Hudson Gateway MLS- weighing in at over 1300 firms, 1650 offices, and 13,000 agents.

In one corner, we have the Hudson Gateway MLS- weighing in at over 1300 firms, 1650 offices, and 13,000 agents.

Just Because the Market is “Hot” Doesn’t Mean Real Estate Agents Have it Easy

The average real estate agent has never worked harder than they have in this market.

That seems contrary to the public perception that rising prices and a “hot” market is when agents have it easy, but extreme conditions aren’t conducive to a leisurely business model.

For example, when an agent sells their new listing the first weekend that it’s active for more than asking, it not only doesn’t mean things are easier for them, it can have a deleterious effect on their bottom line.

Listing agent challenges include:

Other issues are more inside baseball, but the model of the industry has always been predicated on the longstanding idea that carrying a listing for any period of time will develop new prospective client relationships with inquiries on the listing. When the listing is gone the first weekend, that can’t happen. I understand this means little to the consumer, but it’s a factor that can’t be denied.

On the buying side, agents representing prospective purchasers are in trench warfare. Buyer agents in our firm have fewer properties to show their clients, and many of our successful buyers have not hit paydirt until their 4th or 7th attempt to buy. That’s madness. Worse, buyers are selling their souls to get accepted offers by waiving inspections, offering cash to make up for appraisal deficiencies, and in some cases even waiving mortgage contingencies. Surrendering your own security and exposing yourself to that kind of liability is not only stressful and risky, it can be destructive if everything doesn’t go perfectly.

In any industry, volatility is not a welcome thing. Stability, even if it’s considered boring, is a far better market condition. Give me boring any day. Leave the volatility for the Oscars.

Stay tuned for my next post on why this is brutal for consumers as well!